Applying for a personal loan may feel overwhelming, especially if it’s your first time dealing with financial institutions, interest rates, and documentation. But the truth is: once you understand how things work, the entire process becomes smooth, simple, and even stress-free. This guide is written in a friendly, human tone, so you can walk through each step with confidence and apply for a personal loan easily—without confusion or unnecessary worry.

1. Start With a Clear Purpose

Before you think about banks, interest rates, or applications, ask yourself one simple question: Why do I need this loan?

The purpose might be anything—home renovation, wedding expenses, education fees, medical emergencies, or even debt consolidation. Knowing your purpose helps you decide:

how much money you actually need

how quickly you need it

what repayment plan suits you

A clear purpose prevents you from borrowing more than necessary, which protects you from future financial strain.

2. Calculate How Much You Can Comfortably Repay

Many beginners make the mistake of focusing only on the loan amount, not on the repayment. A loan may feel easy to get, but repaying it requires financial discipline.

Ask yourself:

How much can I pay every month without stress?

Do I have a stable monthly income?

Will my income change soon (new job, promotion, business shift)?

A simple rule: Your EMI should not exceed 20–30% of your monthly income.

This keeps your finances balanced and avoids pressure later.

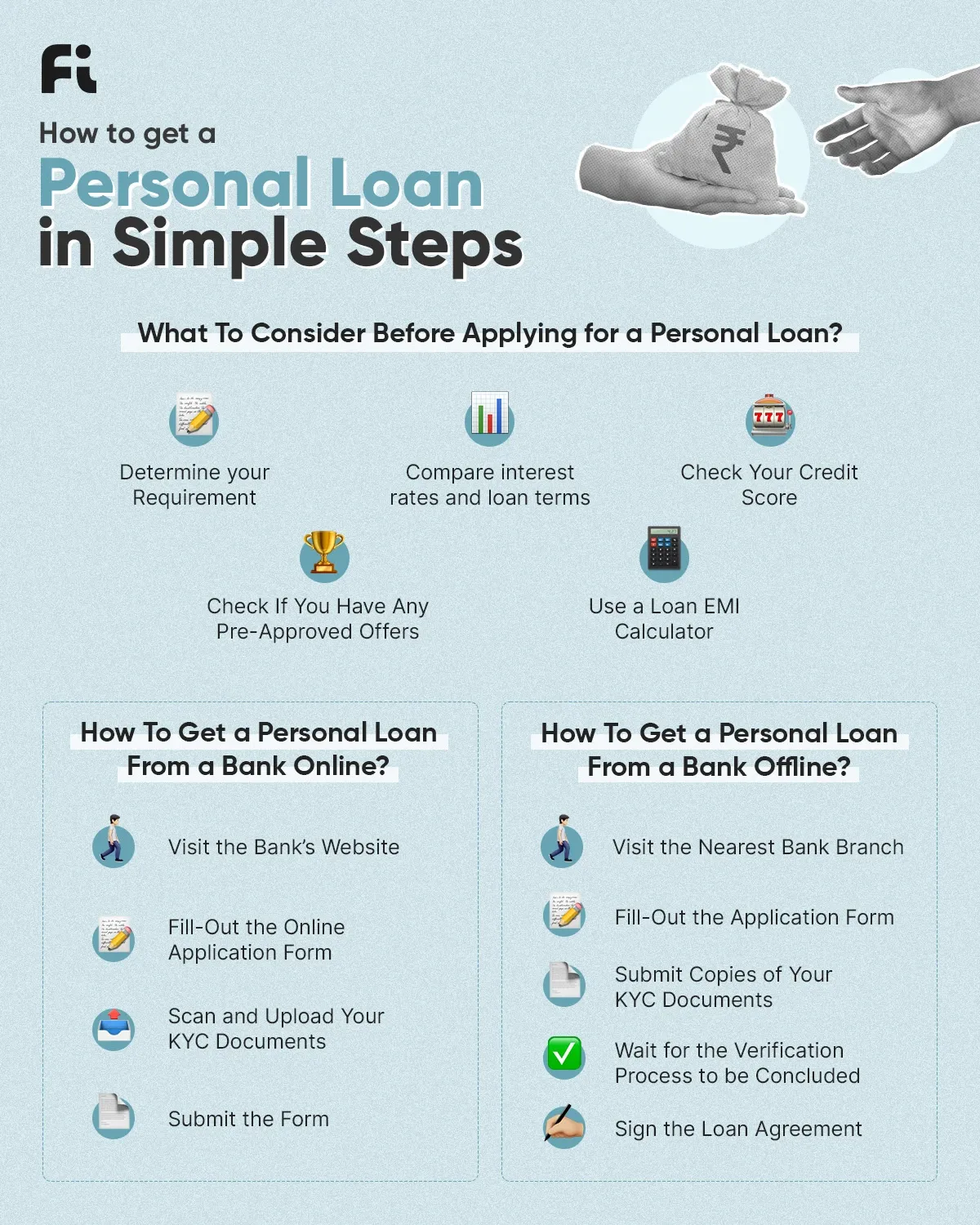

3. Check Your Eligibility Before Applying

Every lender—whether a bank, online finance company, or credit union—has certain eligibility requirements. Understanding these early increases your chances of approval.

Common eligibility factors include:

Age: Usually 21–60

Income: Stable monthly earnings

Employment history: 6 months to 1 year of job stability

Credit score: A good credit record shows you are responsible

Nationality & valid ID: Required for verification

If you already have unpaid loans, high credit card usage, or late payment history, lenders may hesitate. Checking eligibility beforehand saves time and avoids unnecessary rejections.

4. Get Your Documents Ready (This Speeds Up Approval!)

One of the easiest ways to get quick approval is by keeping your documents ready. When everything is complete, lenders process your request faster.

You’ll usually need:

National ID (CNIC/NICOP/Passport)

Recent bank statements (3–6 months)

Salary slips or income proof

Employment letter or business documents

Utility bill or any address proof

Passport-sized photos

Documents may vary slightly depending on lender policies, but having them ready makes you look organized and responsible.

5. Understand Your Credit Score (It Really Matters!)

Your credit score is like your financial reputation. A high score means lenders trust you. A low score means they feel uncertain about your repayment ability.

You can improve your score by:

Paying bills on time

Reducing credit card usage

Clearing old debts

Avoiding multiple loan applications

Even a difference of 20–30 points in your credit score can reduce your interest rate significantly. Beginners often ignore this, but it’s one of the biggest secrets to getting a personal loan easily.

6. Compare Lenders Before Choosing One

Never settle for the first loan offer you get. Every lender has different:

interest rates

fees

processing charges

EMI options

approval timelines

repayment policies

Spend time comparing at least 3–5 lenders. You can check:

online loan comparison websites

bank branches

mobile apps

recommendations from trusted people

Look for the combination of low interest, reasonable fees, and flexible repayment. This single step can save you thousands of rupees in the long run.

7. Apply Online or Visit the Branch

Once you choose your lender, the next step is the application. Thanks to modern technology, applying online is extremely common now. You can fill out the form, upload documents, and track your request from your phone.

If you prefer face-to-face guidance, visit the branch. A loan officer will explain everything and help you complete the application.

Whichever method you choose, make sure:

Your information is accurate

Your contact number and email are correct

Your documents are clear and readable

Mistakes in the application can delay approval or cause rejection.

8. Wait for Verification and Approval

Once your application is submitted, the lender begins their verification process. This usually includes:

Checking your documents

Confirming your employment

Reviewing your bank statements

Checking your credit history

Calling you for confirmation

This process may take from a few hours to a few days depending on the lender.

When everything matches their requirements, your loan gets approved.

9. Receive Your Loan Amount

After approval, the lender sends you an offer letter containing:

loan amount

interest rate

tenure

EMI amount

terms and conditions

Read everything carefully. Once you agree and sign, the loan amount is transferred to your bank account—sometimes instantly, sometimes within 24–48 hours.

10. Repay on Time and Manage Your Loan Wisely

Getting a loan is only half the journey—repaying it responsibly is the real key.

Here’s how to manage it:

Set reminders for EMI dates

Enable auto-debit to avoid late fees

Avoid taking new loans unnecessarily

If you can, repay early to reduce interest

Keep a small savings amount for emergencies

Timely repayment keeps your financial record clean and boosts your credit score.

Final Thoughts

Getting a personal loan easily doesn’t require professional financial knowledge. It just needs clarity, awareness, and a little preparation. When you understand how much you need, compare lenders wisely, keep documents ready, and repay responsibly, the entire loan process becomes smooth and stress-free.

A personal loan should help you—not burden you. Borrow smart, repay smart, and stay financially confident