A personal loan can be a great financial solution when you need extra funds for emergencies, home renovations, weddings, medical bills, education, or any other personal expense. Banks offer personal loans with flexible repayment options, but the process can feel confusing—especially for first-time borrowers.

To make things easier for you, here is a simple, clear, and humanized step-by-step guide that explains exactly how to get a personal loan from a bank.

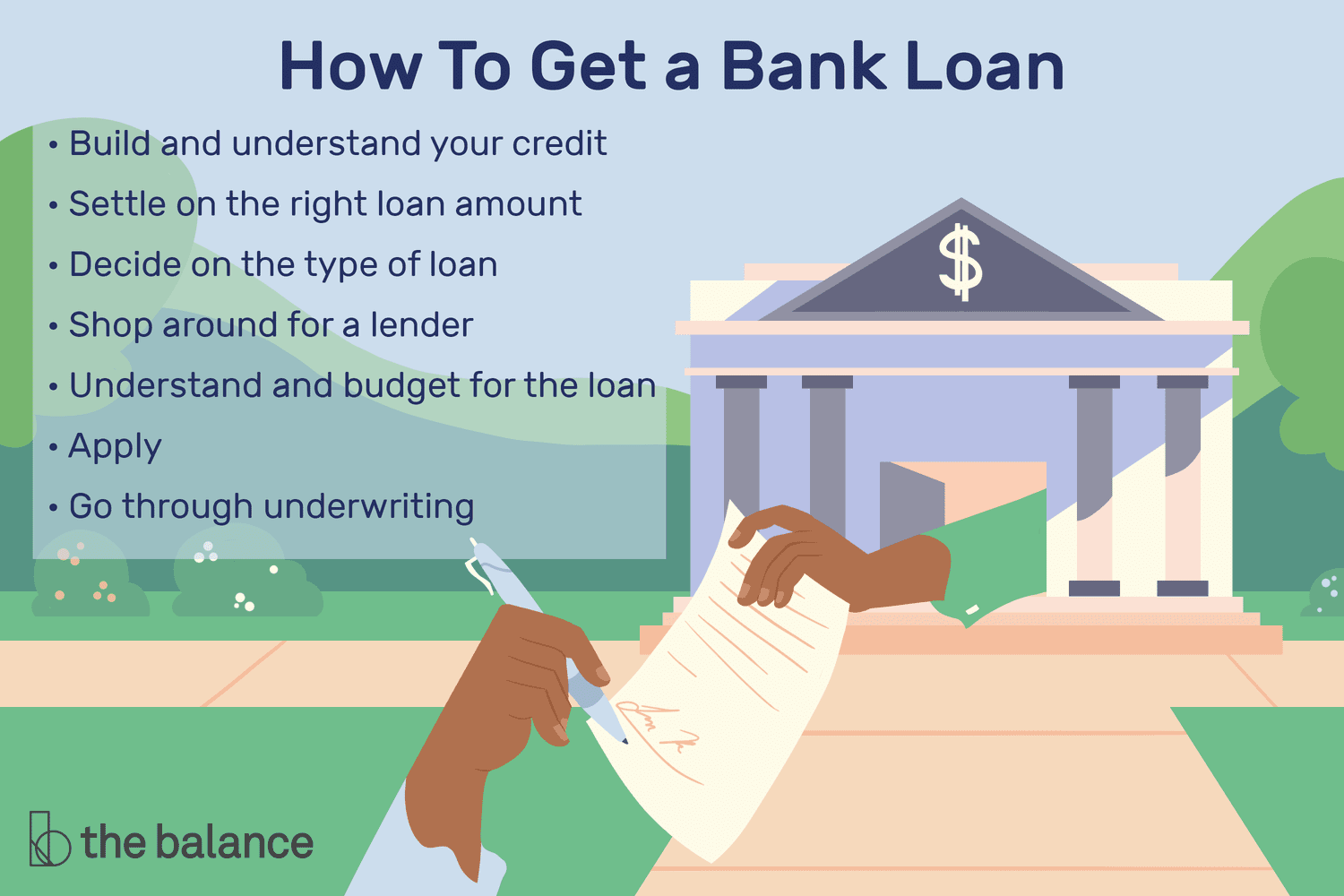

1. Understand What a Personal Loan Is

Before applying, it’s important to know what a personal loan really means.

A personal loan is a type of unsecured loan, which means you don’t need to provide any collateral like property, car, gold, or other assets. Because it’s unsecured, the bank approves it based on:

Your salary or income

Credit score and repayment history

Your job stability

Banking relationship

You receive a lump sum amount and repay it in fixed monthly installments (EMIs).

2. Determine Your Loan Requirement

The first step is to be clear about how much loan amount you need. Many people either borrow too little and face shortages later, or borrow too much and struggle with repayment.

Ask yourself:

What is the exact purpose of this loan?

How much money do I truly need?

Can I repay the amount comfortably each month?

Getting clarity at the beginning will help you avoid unnecessary financial pressure in the future.

3. Check Your Eligibility Before Applying

Every bank has its own eligibility criteria. While they may differ slightly, the major factors are always similar:

Common Eligibility Requirements:

Minimum age (usually 21–60 years)

Stable job or business

Monthly income requirement

Good credit score (650+ preferred)

6–12 months of job stability (for salaried persons)

1–2 years business proof (for self-employed persons)

Checking your eligibility beforehand saves you from rejection and unnecessary inquiries on your credit report.

4. Verify Your Credit Score

Your credit score is one of the most important factors in loan approval. It tells the bank how responsibly you repay past loans or credit card bills.

Why Credit Score Matters?

Higher credit score = Higher chances of approval

You may get a lower interest rate

Faster loan disbursement

Better loan terms and flexibility

If your score is low, try to improve it before applying by clearing old dues and paying bills on time.

5. Compare Banks and Their Loan Offers

Do not apply for a loan with the first bank you see. Every bank offers different interest rates, loan tenures, processing fees, and benefits.

Things to Compare:

Interest rate (APR)

Maximum loan amount

Loan tenure options

Processing fee

Insurance charges

Prepayment or early settlement penalty

Any hidden charges

Even a small difference in interest rate can save you a lot of money over the full duration of the loan.

6. Use EMI Calculators to Plan Better

All banks have EMI calculators on their websites. These tools help you understand:

Your monthly EMI

Total amount payable

Total interest paid

Impact of different tenures

It’s very important to know whether the monthly installment fits your budget before applying.

7. Gather Required Documents

Banks require some standard documents for verification. Keeping them ready in advance makes the process faster.

Common Required Documents:

✔ CNIC / National ID

✔ Salary slips (last 3–6 months)

✔ Bank statements (last 6–12 months)

✔ Employment letter (for salaried individuals)

✔ Income tax documents (if required)

✔ Proof of business (for self-employed)

✔ Utility bill or address proof

Make sure all documents are clear, updated, and valid.

8. Visit the Bank or Apply Online

Most banks now offer two methods to apply for a personal loan:

A. Apply by Visiting the Bank

Meet a loan officer

Ask for loan details

Submit your forms and documents

Get guidance through the entire process

This method is helpful if you want a human explanation about terms and conditions.

B. Apply Online

Visit the bank’s official website

Fill out the application form

Upload documents

Get instant eligibility check

Quick approval process

Online applications are faster and more convenient.

9. Wait for Verification and Approval

Once you submit your application, the bank begins the verification process. They will:

Verify your job or business

Check your credit history

Review your bank statements

Analyze your repayment capacity

If everything is correct, they will approve your loan. Sometimes the bank may request additional documents—this is normal.

10. Loan Offer and Agreement Signing

After approval, you will receive a loan offer. It includes:

Loan amount

Tenure

Interest rate

EMI amount

Total payable amount

Penalties and charges

Carefully read the entire agreement. Make sure you understand all terms. If something is unclear, ask the bank representative before signing.

Never sign without reading.

11. Loan Disbursement (Money Transfer)

Once the agreement is signed, the bank transfers the loan amount to your:

Bank account

Salary account

Or issues a cheque (rarely)

This usually happens within 24–72 hours after final approval.

12. Repayment Through Monthly EMIs

After receiving the loan, your repayment begins as per the schedule. The EMI is automatically deducted from your bank account each month.

Tips for smooth repayment:

Maintain sufficient balance

Never miss an EMI

Avoid late payments

Try to prepay when possible (if penalty-free)

Timely repayment will keep your credit score healthy and improve your future loan chances