Getting a loan feels simple in theory — you apply, wait for verification, and get the money. But in reality, many people face repeated rejections from banks and loan apps. Some apply again and again, hoping for a different result, but the outcome remains the same: “Your loan application has been declined.”

If this sounds familiar, you are not alone. There are millions of people who never get loan approval, not because they are bad borrowers, but because they are unaware of the reasons behind rejection.

This article explores the real, practical, human reasons why some people struggle to get approved — and what you can do to improve your chances.

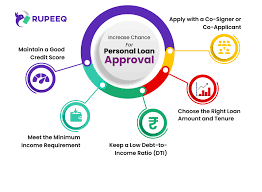

1. Poor or No Credit Score History

One of the biggest reasons behind loan rejection is a low credit score or zero credit history.

Why it happens:

Late EMI payments

Credit card overdue

Taking too many small loans

Not having any previous credit record

Banks trust people who have shown good repayment behavior in the past. If you never took a loan before, the bank has no proof you can repay one now.

Human Tip:

Start by building small credit. Use a credit card wisely or take a small secured loan. Build a positive repayment history for 6–12 months.

2. Unstable or Irregular Income

Lenders want to see stable monthly income.

People with irregular income — such as freelancers, gig workers, daily wage earners, or small business owners — often get rejected.

Why lenders reject:

Income changes monthly

No fixed salary statement

High financial risk

Even if you earn well, lenders prefer consistency over high amounts.

Human Tip:

Show at least 6–12 months of consistent bank deposits, even if income varies. Banks love stability more than numbers.

3. High Debt-to-Income Ratio

If your income is Rs 50,000 but your existing EMIs take away Rs 25,000, your debt-to-income ratio becomes too high.

Lenders hesitate because:

Too much of your income is already committed

Risk of default is higher

Borrower may struggle to pay more EMIs

Human Tip:

Keep your total EMIs below 40% of your income. If already high, close some loans before applying for a new one.

4. Multiple Loan Applications in a Short Time

Many people apply to:

3 banks

5 loan apps

2 NBFCs

1 credit card

…all within the same month.

This damages your credit score.

Every time you apply, the lender checks your credit report, which creates a hard inquiry. Too many inquiries look like you’re financially desperate.

Human Tip:

Apply only to one or two reliable lenders. Too many applications equal instant rejection.

5. Incorrect or Incomplete Documentation

A huge number of applications are rejected because of simple mistakes like:

Wrong CNIC / ID card number

Unclear bank statements

Fake salary slips

Mismatched signatures

Missing documents

Banks and apps cannot approve incomplete or suspicious documents.

Human Tip:

Double-check everything. Ensure your documents are clean, updated, and clearly readable.

6. Unverifiable Employment Details

If your employer cannot be verified, your loan is likely to be rejected.

Common causes:

Working in a very small business

No official HR department

Your employer doesn’t respond

You provided an incorrect HR number

Lenders need confirmation that you actually work where you claim.

Human Tip:

Provide correct HR details, office numbers, and proof of employment. Even a work letter helps.

7. Your Bank Account Shows Financial Stress

Yes, lenders check your bank statement carefully. They look for:

Negative balances

Low balance throughout the month

Frequent withdrawals

No healthy savings

Too many transfers from loan apps

These signs make you look financially unstable.

Human Tip:

Keep your bank account healthy. Maintain a minimum balance, avoid unnecessary withdrawals, and show proper income deposits.

8. You Work in a High-Risk Industry

Some industries are considered unstable, seasonal, or unpredictable.

Examples:

Real estate agents

Commission-based jobs

Small shop workers

Daily labor work

Contract employees

Banks prefer customers with long-term job security.

Human Tip:

Show additional proof like:

Side income

Rental income

Freelancing earnings

This reduces perceived risk.

9. Age-Related Restrictions

People too young (18–21) or too old (above 60) often face rejection.

Why?

Lenders believe the risk is higher.

Human Tip:

If you are young, start by building credit with small loans. If older, apply for shorter-tenure loans.

10. Suspicious or Inconsistent Information

If your application has mismatched information such as:

Different salary in bank account vs salary slip

Address doesn’t match

Job title differs from company records

Fake documents

The result is instant rejection.

Human Tip:

Be 100% honest. Lenders cross-check everything digitally.

11. Poor Relationship With the Bank

If you have a history of:

Returned cheques

Overdraft misuse

Account inactivity

Old loan defaults

Your bank will hesitate to approve new credit.

Human Tip:

Rebuild trust by maintaining a clean account for 6–12 months.

Conclusion: Why Some People Never Get Loan Approval

Loan rejection is not the end — it’s feedback.

Most people never get approval because they don’t understand the system. Loans are not just about asking for money; they are about proving that you can repay it reliably.

To improve your chances:

Build a good credit score

Maintain stable income

Apply with correct documents

Control your existing loans

Keep your bank account healthy

Apply only to trusted lenders

With the right strategy and patience, anyone can turn “Rejected” into “Approved.”